Resale markets will show signs of recovery but remain below long-term averages.

Housing starts will continue to slow down in 2026, with a more significant decline expected in 2027 – 2028.

Rental market affordability will continue to improve as high vacancies and slower rent growth persist.

Lower condominium presale activity will limit new condominium construction over the next 3 years.

British Columbia’s labour market expected to recover in 2026, but demographic factors will weigh on housing markets

British Columbia’s (B.C.) economy is expected to improve in 2026 after limited growth in 2025. As forecasted in our Housing Market Outlook summer 2025 update, a weak labour market and trade volatility were the main factors impacting B.C.’s economy in 2025.

In 2026, employment conditions will improve with unemployment trending lower and labour force growth slowing. However, slower public sector job growth is likely to limit some of this recovery, keeping unemployment rates historically high. Wage growth is expected to pick up as the labour market tightens, after slowing in 2025.

We expect B.C. to experience a smaller negative impact from global trade volatility compared to other provinces with larger manufacturing sectors. U.S. lumber tariffs and weaker U.S. homebuilding activity may affect the softwood lumber industry, but these impacts will likely be limited to Northern and Interior markets, rather than the Lower Mainland and South Coast.

The sectors tied to technology and professional services have been B.C.’s fastest growing over the past decade (Figure 1). We expect these sectors to play an even larger role in the coming years. Employment and investment in these sectors will drive some housing demand, especially in major urban centres.

Figure 1: Employment in B.C. Has Become More Concentrated in Professional and Tech Sectors

Full-Time Employment, Select Industries, 2014 = 100

Construction: 121.9

Real estate and rental and leasing: 109.3

Health care and social assistance: 122.5

Forestry, fishing, mining, quarrying, oil and gas: 94.4

Professional, scientific and technical services: 125.1

2018

Source: CMHC, Statistics Canada

Text version (Figure 1)

Full-Time Employment, Select Industries, 2014 = 100| Year | Construction | Real estate and rental and leasing | Health care and social assistance | Forestry, fishing, mining, quarrying, oil and gas | Professional, scientific and technical services |

|---|

| 2014 | 100 | 100 | 100 | 100 | 100 |

|---|

| 2015 | 101.7 | 83.9 | 106.8 | 101.4 | 109.7 |

|---|

| 2016 | 107.2 | 91.5 | 111.4 | 99.2 | 112.7 |

|---|

| 2017 | 118.8 | 111.5 | 116.5 | 101.0 | 116.9 |

|---|

| 2018 | 121.9 | 109.3 | 122.5 | 94.4 | 125.1 |

|---|

| 2019 | 124.2 | 115.4 | 121.7 | 87.1 | 135.3 |

|---|

| 2020 | 111.3 | 110.7 | 122.2 | 77.9 | 138.2 |

|---|

| 2021 | 112.7 | 103.4 | 133.1 | 92.4 | 153.4 |

|---|

| 2022 | 116.5 | 104.9 | 143.4 | 89.9 | 164.4 |

|---|

| 2023 | 116.6 | 114.9 | 150.0 | 96.6 | 170.9 |

|---|

| 2024 | 123.5 | 127.6 | 160.0 | 101.8 | 176.7 |

|---|

| 2025 | 129.5 | 124.4 | 160.2 | 84.9 | 180.2 |

|---|

International migration to B.C. will continue to decline in 2026, as seen in 2025. This decline is largely due to slower non-permanent resident flows. As a result, rental and investor demand will be impacted, limiting resale activity. On the other hand, improving affordability in Vancouver and Victoria over the past year will reduce the number of people leaving these regions for other parts of B.C. and other provinces.

Slower rental demand and rising costs will decrease new home starts

New home construction in B.C. markets will trend lower in 2026, following strong activity in the apartment segment in 2025. This will be a departure from our summer forecast, where we forecasted a slight increase in 2026. New home construction will continue to decrease later in the forecast period, due to weak supply and demand.

Apartment construction in urban centres across the province has been strong in recent years, driven by favourable policy and financing incentives for rental supply and consistent demand. However, construction conditions have become increasingly difficult, with builders citing rising costs as a significant barrier for new construction.

A significant decline in condominium presales, in Vancouver and Victoria, has stalled many planned projects. We expect more condominium projects to be postponed or cancelled in 2026, with these effects extending into 2027 and 2028.

Rental construction will also start to slow in the second half of 2026, as developers respond to higher vacancy rates and slower rent growth that we observed in our 2025 Rental Market Report. While many projects currently in the pipeline will contribute to housing starts in 2026, we expect a continuous slowdown in project proposals and construction into 2028. Similar to condominium construction, developers face challenges from high material and regulatory costs, weaker rent growth and slower absorptions, making new rental projects increasingly difficult.

Ground-oriented construction, representing single-detached, semi-detached and townhomes, will stay relatively stable in 2026, with some growth expected in 2027 and 2028. While single-detached will continue to be weak in the Vancouver CMA, these homes will still be in demand, especially in more affordable regions like Victoria and Abbotsford. At the same time, demand for denser ground-oriented homes will increase in the Vancouver CMA, as they offer a more affordable option.

Resales are expected to increase moderately in 2026

After a historically weak 2025, the resale markets in Vancouver and Victoria will show some recovery in 2026. However, this rebound will likely remain below historical averages. Since our summer Housing Market Outlookupdate, resale markets have remained persistently weak. Despite lower mortgage rates in 2025, a weaker labour market and ongoing economic uncertainty kept resales slow. High accumulated listings and a softer rental market also contributed to this slowdown.

A stronger labour market and continued low mortgage rates will support more resales in 2026. Expectations of interest rate increases in 2027 may prompt some waiting buyers to enter the market sooner. Improved affordability for higher-priced homes will boost resales, but entry-level home prices are expected to stay steady.

Sales growth will likely slow in 2027 and 2028 in Vancouver and Victoria due to ongoing demographic and pricing challenges. Softer rental markets will dampen individual investor activity, especially in the condominium market.

Average prices supported by rebound in activity, but growth will be limited

Resale prices are expected to rise moderately in 2026, supported by higher sales as markets shift toward more balanced conditions. Beyond 2026, price growth will likely remain low, with average prices unlikely to reach the highs seen in recent years. Rising mortgage rates expected in 2027 will limit increases in borrowing capacity (Figure 2), further limiting price growth during that time and beyond.

Figure 2: Borrowing Capacity Limits Will Limit Price Growth in B.C. Markets

Note: Borrowing capacity calculated using 5 year fixed mortgage rate assumptions and the average wage of a full-time salaried worker in BC aged 25 – 54.

Text version (Figure 2)

Despite a slower resale environment, prices in Vancouver and Victoria have remained relatively stable, especially compared to declines in Toronto. This stability will likely persist, but price adjustments are expected in specific higher-priced areas and home types within these regions. Recent price declines and lower mortgage rates have made ownership more favourable. Some current renters will be more incentivized to transition to homeownership over the next year, as the gap between owning costs and renting costs shrink (Figure 3).

Prices in urban areas will remain stronger than those further away. Efforts to bring employees back to offices will increase demand for homes closer to city centres. Meanwhile, improved affordability in areas further from urban centres will slow interprovincial population outflows, supporting some demand in those regions.

The mix of homes sold will also support average prices. With a large supply of condominiums expected to be completed in the next year, those entering the resale market will likely have higher prices, which will help support average prices. However, real appreciation of homes is unlikely to fully recover from recent declines.

Figure 3: The Gap Between Owning and Renting an Apartment Has Shrunk in Metro Vancouver ($)

Note: Carrying cost includes assumptions for a 20% downpayment, 25-year amortization, the prevailing discounted 5 year fixed mortgage rate, property taxes, and condo fees.

Rental markets will see elevated vacancies maintained for 2026

Vacancies rose sharply in 2025 in most centres across the province, with Vancouver reaching its highest levels in over 30 years. We expect these elevated vacancy rates to persist in 2026 into 2028. Recent changes to immigration policy have reduced rental demand across the province, while many new rental units are set to be completed in the next few years.

We expect international migration to remain slower over the next few years, at least until 2028. Since migrants are a primary source of demand for rental units in major centres, the uptake of new rental inventory will likely stay below previous levels. Youth unemployment will also be a significant factor. High unemployment rates are preventing many young people from entering the rental market, leading them to either share housing with a roommate or stay with their parents. As the economy recovers, delayed household formations could lead to an increase in rental demand.

High vacancies will keep average rent growth slow. As we saw in 2025, average rent growth was at the lowest rate we’d seen in over a decade, outside of the pandemic period. Rent growth on turnover is likely to continue slowing, while rent increases for existing tenancies will likely be close to zero. However, the influx of newly completed rental units expected to enter the rental market will raise average rents due to their higher prices.

Affordability will continue to improve as rent growth remains stalled and renters have more options available.

This forecast is subject to risks

Resale markets in B.C may experience extended downturns in both price and volume, if labour markets do not meaningfully improve in the next year. In that scenario, prices will likely remain flat or move lower to adjust for lower demand. Mortgage rates rising more and earlier than expected will also negatively impact resale activity in the province.

The current cross-border and international trade environment adds risk to the forecast. If more negative outcomes to trade are imposed on B.C specific exports like lumber and energy, local economies will be impacted. Similarly, changes to domestic policy in the United States may impact purchasing behaviours and rental demand of dual citizens and cross-border workers.

On the other hand, if international migration patterns reverse, and inflows return to historical averages, housing demand will increase, especially for rental markets. This would lead to lower vacancy rates and higher rent growth.

Vancouver

Key highlights

Resale market will rebound moderately as activity moves toward more balanced conditions.

Home prices will stabilize in 2026, with slight increases possible. However, significant growth is unlikely in the following years.

Housing starts will continue to decline due to high construction costs and weak demand.

Vacancies will remain high as rental units started over the past 4 years enter the market, slowing rent growth and improving affordability.

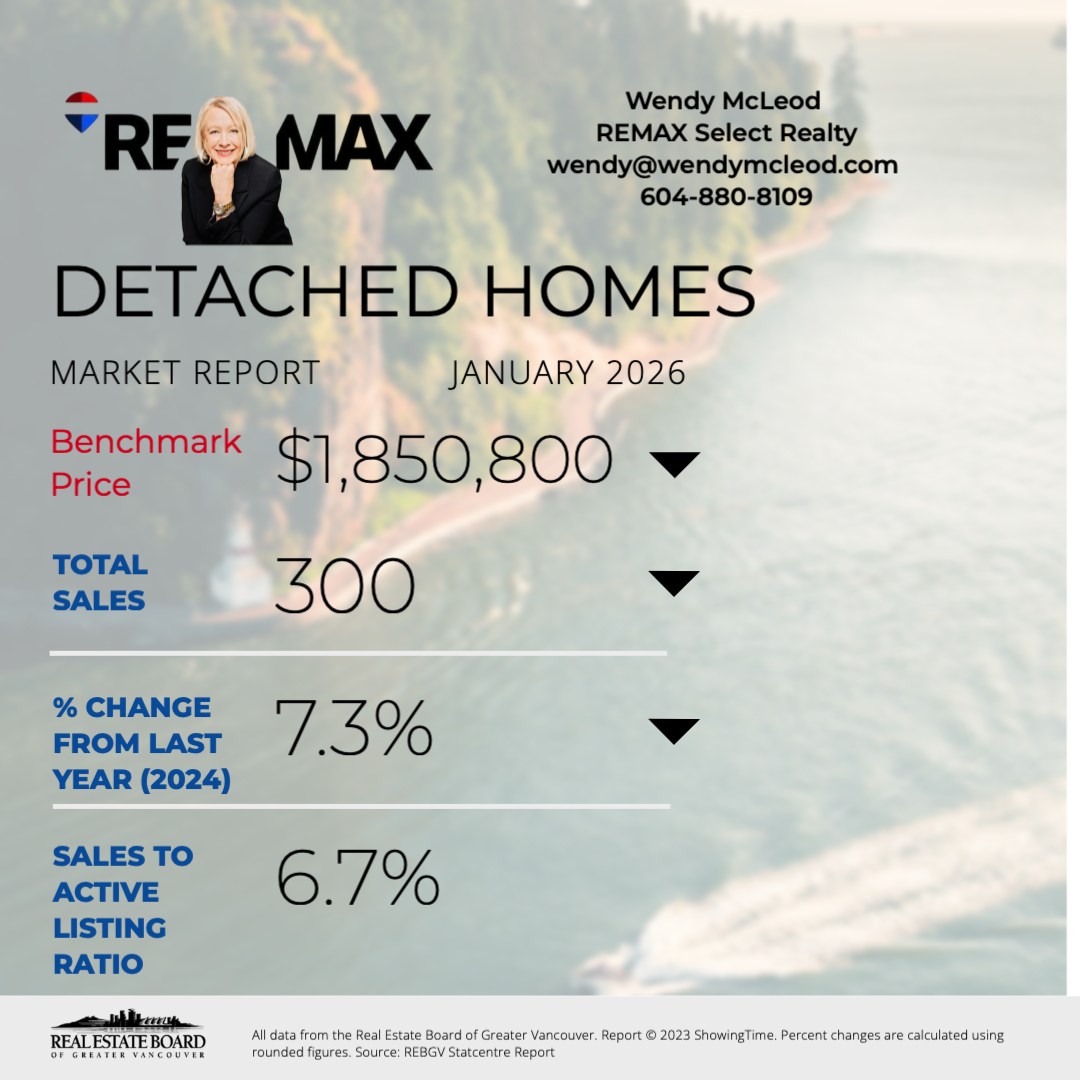

Resale activity in the Vancouver CMA will recover moderately in 2026 after the slowest resale rate in over 20 years. While sales activity will see moderate growth later in 2027 and 2028, it will remain below the 10-year average throughout the forecast period.

This recovery will likely be concentrated in areas closer to the city centre, where prices have remained resilient over the past year, especially for apartment condominiums. On the other hand, newer condominiums south of the Fraser may require further price adjustments before sales improve. The push for employees to return to the office is a key factor driving this difference.

For ground-oriented attached homes, such as semi-detached and townhomes, North Fraser communities like Coquitlam are expected to perform well due to their competitive pricing and commuting distance from downtown. Price growth of single-detached homes across the region will be limited due to their high levels, but these prices are unlikely to decline further as many have already reverted to 2021 levels.

New home construction for ground-oriented housing will follow similar geographical patterns in the resale market. In the City of Vancouver, new single-detached construction will continue to be rare, with existing homes being replaced by semi-detached or denser housing types. Multiplex construction will continue but may slow as opposition to these forms grows in some Metro Vancouver cities. Construction of more common forms, like townhomes, will grow moderately over the next few years.

Declining apartment starts will be the main driver in lower total starts over the forecast period. Weak condominium apartment sales in recent years and uncertainty about future price growth have significantly slowed presales. With very few presales, developers will find it difficult to proceed with new condominium projects, resulting in limited apartment condominium starts over the next 2 years.

We also expect the recent trend of growth in rental apartment construction to decline in the second half of 2026. Softer rental market conditions throughout Metro Vancouver will make it harder for projects to move past the planning stages as viability becomes more difficult. While some municipal governments, like the City of Vancouver, are proposing policies to reduce development cost charges and boost apartment construction, these changes are unlikely to result in housing starts until late in 2027.

Vacancies will remain high as record numbers of under-construction rental apartments are completed over the next 3 years. Most of these units are concentrated in and near the City of Vancouver, where demand for rental homes closer to the downtown core will meet some of this supply. Rent growth in Metro Vancouver will continue to be limited. Some landlords may lower asking rents or offer incentives to compete with the growing availability of supply. As a result, rental affordability will continue to improve over the next 3 years.

Forecast Summary (Vancouver CMA)| Date | New Home Market Starts | Resale Market | Rental Market |

|---|

| Ground-oriented | Apartments | Total | MLS® Sales | MLS® Average Price ($) | Vacancy rate (%) | Average Rent Two Bedrooms ($) |

|---|

| 2023 | 5,668 | 27,576 | 33,244 | 36,377 | 1,216,622 | 0.9 | 2,181 |

|---|

| 2024 | 4,830 | 23,282 | 28,112 | 36,099 | 1,234,969 | 1.6 | 2,314 |

|---|

| 2025 | 5,341 | 21,844 | 27,185 | 30,818 | 1,183,970 | 3.7 | 2,363 |

|---|

2026 (F)

Low | 5,300 | 17,400 | 22,700 | 27,900 | 1,111,000 | 4.1 | 2,381 |

|---|

2026 (F)

High | 6,400 | 21,200 | 27,600 | 40,000 | 1,348,000 |

|---|

2027 (F)

Low | 4,800 | 16,200 | 21,000 | 29,300 | 1,111,000 | 4.2 | 2,443 |

|---|

2027 (F)

High | 6,900 | 18,700 | 25,600 | 42,900 | 1,353,000 |

|---|

2028 (F)

Low | 4,700 | 16,300 | 21,000 | 31,800 | 1,124,000 | 4.0 | 2,516 |

|---|

2028 (F)

High | 7,900 | 17,600 | 25,500 | 47,600 | 1,373,000 |

|---|

Source: Greater Vancouver REALTORS, Fraser Valley Real Estate Board, CMHC

The forecasts included in this document are based on information available as of January 15, 2026.

Victoria

Key highlights

Resale activity will pick up in 2026 as buyers act ahead of expected higher mortgage rates in 2027, while high inventory levels will moderate price growth.

New construction will continue to rise in 2026, led by rental apartment projects, before slowing down as condominium demand softens.

Rental market vacancies will remain high in 2026 as new supply outpaces demand, limiting rent growth and improving affordability.

Sales activity in the Victoria CMA is expected to recover modestly in 2026 after slowing in late 2025. This recovery will be supported by low interest rates and buyer urgency ahead of anticipated rate hikes in 2027. This rebound will provide some near-term momentum in 2026. However, growth is expected to soften through 2027 and 2028 as slower population growth and labour market challenges begin to reduce demand.

Elevated inventory levels will give buyers more options, with many delaying purchases in hopes of further price moderation. Price growth will increase slightly in 2026, driven by improved sales activity, before stabilizing over the rest of the forecast period. While Victoria’s market has avoided the significant softening seen in larger centres, growing new-home inventory and economic uncertainty will limit the upside potential of price growth.

We forecast housing starts to rise in 2026, marking another year of growth. However, this momentum will slow through 2027 and 2028 as developers take a more cautious approach amid softening market conditions. Rising interest rates and potential tariffs on building materials will add cost pressures, further constraining project viability.

Apartment construction will continue to drive new supply, with starts increasing in 2026 before moderating later in the forecast period. Government incentives and a structural shift toward higher-density housing continue to support this segment, but weak condominium demand and softening rental market conditions will limit large projects.

Ground-oriented construction will only increase marginally in 2026, as developers pivot away from lower-density construction. Elevated unabsorbed inventory, particularly in row and semi-detached units, combined with softer demand, will discourage new starts in this segment.

We expect rental market conditions to soften further in 2026. A significant number of new purpose-built rental units will be completed, adding to supply at a time when demand is weakening. Declining asking rents and increased incentives from landlords reflect growing competition for tenants, particularly in higher-priced units. Slower population growth and labour market weakness will continue to challenge rental demand, improving affordability over the next 3 years.

Forecast Summary (Victoria CMA)| Date | New Home Market Starts | Resale Market | Rental Market |

|---|

| Ground-oriented | Apartments | Total | MLS® Sales | MLS® Average Price ($) | Vacancy rate (%) | Average Rent Two Bedrooms ($) |

|---|

| 2023 | 752 | 4,238 | 4,992 | 5,934 | 982,350 | 1.6 | 1,839 |

|---|

| 2024 | 779 | 3,411 | 4,185 | 6,582 | 973,702 | 2.6 | 1,993 |

|---|

| 2025 | 908 | 3,951 | 4,859 | 6,605 | 1,011,263 | 3.3 | 2,120 |

|---|

2026 (F)

Low | 750 | 3,750 | 4,500 | 6,200 | 1,007,000 | 3.6 | 2,190 |

|---|

2026 (F)

High | 1,000 | 4,950 | 5,950 | 7,800 | 1,071,200 |

|---|

2027 (F)

Low | 600 | 4,050 | 4,650 | 5,950 | 988,700 | 3.4 | 2,340 |

|---|

2027 (F)

High | 1,100 | 5,050 | 6,150 | 8,330 | 1,164,300 |

|---|

2028 (F)

Low | 500 | 4,100 | 4,600 | 5,670 | 963,900 | 3.0 | 2,410 |

|---|

2028 (F)

High | 1,200 | 4,900 | 6,100 | 8,850 | 1,257,700 |

|---|

Source: CREA, CMHC

The forecasts included in this document are based on information available as of January 15, 2026.

What’s next for Canada’s housing market?

Join Kevin Hughes, Deputy Chief Economist, on our In-House podcast as he unpacks the 2026 Housing Market Outlook. Gain expert insights on economic shifts, affordability challenges and regional trends.

Listen now

Our Chief Economist and Deputy Chief Economists

Our Chief Economist and Deputy Chief Economists lead a cross-country team of housing economists, analysts and researchers who strive to improve understanding of trends in the economy, housing markets, and how they impact affordability.

Mathieu Laberge

Chief Economist and Senior vice-president, Housing Insights

Aled ab Iorwerth

Deputy Chief Economist

Kevin Hughes

Deputy Chief Economist

Tania Bourassa-Ochoa

Deputy Chief Economist